Spring Clean Your Finances

April 22, 2025

Health is our most valuable asset. Without good health, nothing else really matters, does it? Likewise, mental health is so much more than just wellbeing; it forms the foundations of how we think, feel, and function – all day and every day.

Under (Mental Health) Pressure

We talked recently about the impact of money worries and debt problems on mental health, and how we can help. However, it’s vital to recognise that people whose mental health is suffering are more likely to fall into debt. When our mental health is under par, every aspect of life can be affected, including our financial stability. Yet we rarely talk about how conditions like anxiety, depression, PTSD and even learning differences like ADHD can lead directly and indirectly to money problems and, ultimately, debt.

From an early age, it’s instilled into us to work hard and try our best. We’re taught that to succeed and to stay productive is vital. What happens when we can’t? Sometimes, simply getting out of bed feels impossible. It’s hard to even function. How can we work and plan and perform? Trying to budget seems like an insurmountable hurdle. Even opening the post can fill us with dread, so we avoid it. Mental health challenges can interfere with the basics that underpin our financial security.

Mental Illness and Managing Money

Tasks that once seemed simple – automatic, even – like paying bills on time, managing direct debits, meeting deadlines, or planning for the future, can feel overwhelming when your mental health is suffering. Just as someone with a broken leg struggles to walk, someone with depression may struggle to manage their money. Never underestimate that impact. When our mental health isn’t good, it can feel hard to:

- Perform at work: Anxiety, depression, or burnout might lead to absence, underperformance, or even job loss.

- Communicate confidently: Making calls to banks or creditors can feel impossible.

- Stay on top of finances: Executive dysfunction can make budgeting or bill-paying a real challenge.

- Resist impulsive spending: Certain conditions, like bipolar disorder or ADHD, can include impulsivity or risk-taking, which can lead to spending and gambling.

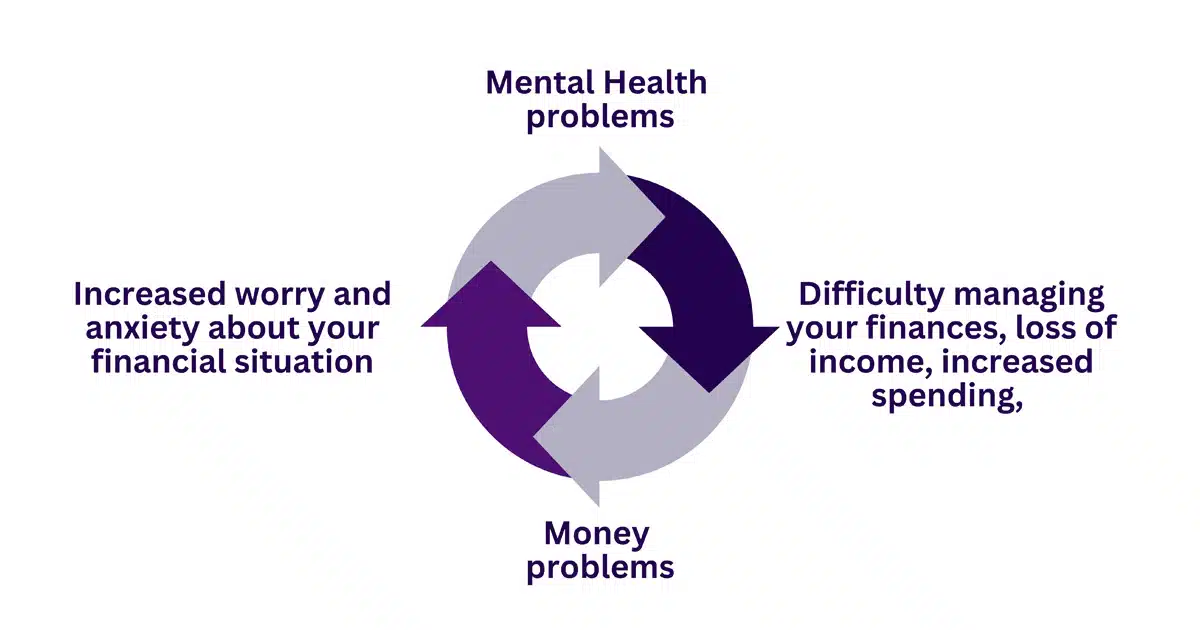

These difficulties can lead to further financial problems and an ongoing vicious circle.

Poor Mental Health and Spending

Mental health struggles can also drive unhealthy financial behaviours. When we’re depressed, we seek ways to feel better. Shopping, eating out, gambling, or gifting can be used as coping mechanisms. In reality, they’re little more than a momentary escape, a quick fix to lift the mood or gain a sense of control. But beware. It starts small: a little treat here, a splurge there. But over time, this kind of spending can become a habit – one which is hard to break. Worse, any minor lift in mood soon crashes down again.

- Low mood or depression can lead to lethargy, apathy and avoidance. This can mean ignoring bills, missing payments, or letting things spiral.

- Anxiety can cause panic-spending or excessive worry about money, even when it’s not warranted.

- Trauma and PTSD can create feelings of insecurity, leading to hoarding, over-giving, or neglecting basic needs.

- In severe mental health cases, mania may result in episodes of excessive or risky spending, later followed by shame and regret, thus further cementing the mental health struggles.

This means that not only can mental health difficulties cause or contribute to debt problems, but can even lead to overspending, compounding the issue further.

Mental Health Drives Financial Strain – or Gain

Such is the harsh reality. Mental health issues can quietly, or sometimes dramatically, unravel financial stability. It’s not always obvious from the outside, we tend to hide both mental health and financial concerns. Behind the scenes, many of us are battling both internal chaos and external consequences:

- Missed rent or mortgage payments due to lost income or executive dysfunction.

- Mounting debt from impulse purchases, emotional spending, avoidance or disorganisation.

- Loss of benefits or entitlements through difficulty navigating paperwork or making appointments.

- Isolation from support networks, increasing the burden due to trying to cope alone.

These challenges don’t happen in a vacuum. Life is harder, more stressful, and more expensive when mental health isn’t supported. And without help, as we’ve explained, this creates a vicious circle whereby mental illness leads to money problems, which worsen mental illness, and so on. And so on…

Stop the Stigma – Seek Help

Mental illness can have an acute financial cost. Why, then, are we often too ashamed to seek support or even advice? There is no shame in struggling. It can happen to anyone. Mental health is health, and the challenges it creates are real. Just as you’d seek help for a broken arm, you can need support when your mind is hurt. That’s especially true when it’s affecting your finances too.

It’s time to break the cycle. We can help you do it:

- You are not alone. Many people experience money troubles linked to their mental health.

- Talk to someone. Whether it’s a friend, your GP, a therapist, or financial advisor, opening up is the first step. If you’re not sure where to find the right advice, our Support Hub is invaluable, and we can signpost you.

- Access specialist support. There are organisations offering advice that’s sensitive to mental health challenges. Again, we can help you find and access them or you can visit the National Support Network.

- Register your vulnerability. This can make an enormous difference to how organisations and creditors approach you and is vital when your mental health is at risk.

- Create small, achievable, sustainable changes. Even one manageable step, like sorting your post, or tracking one expense is progress.

You don’t have to tackle this alone. We’re here to help you take control, one step at a time. Contact us today and let’s find you the help you deserve.

{kind=link}

{kind=link}

{kind=link}

{kind=link}